What is happening in the British property market?

The doom and gloom of the national newspaper headlines regarding the UK property market would make you think Armageddon has arrived. Newspaper headlines imply the housing market has crashed. But has it really? Let’s look at thing in a bit more detail….

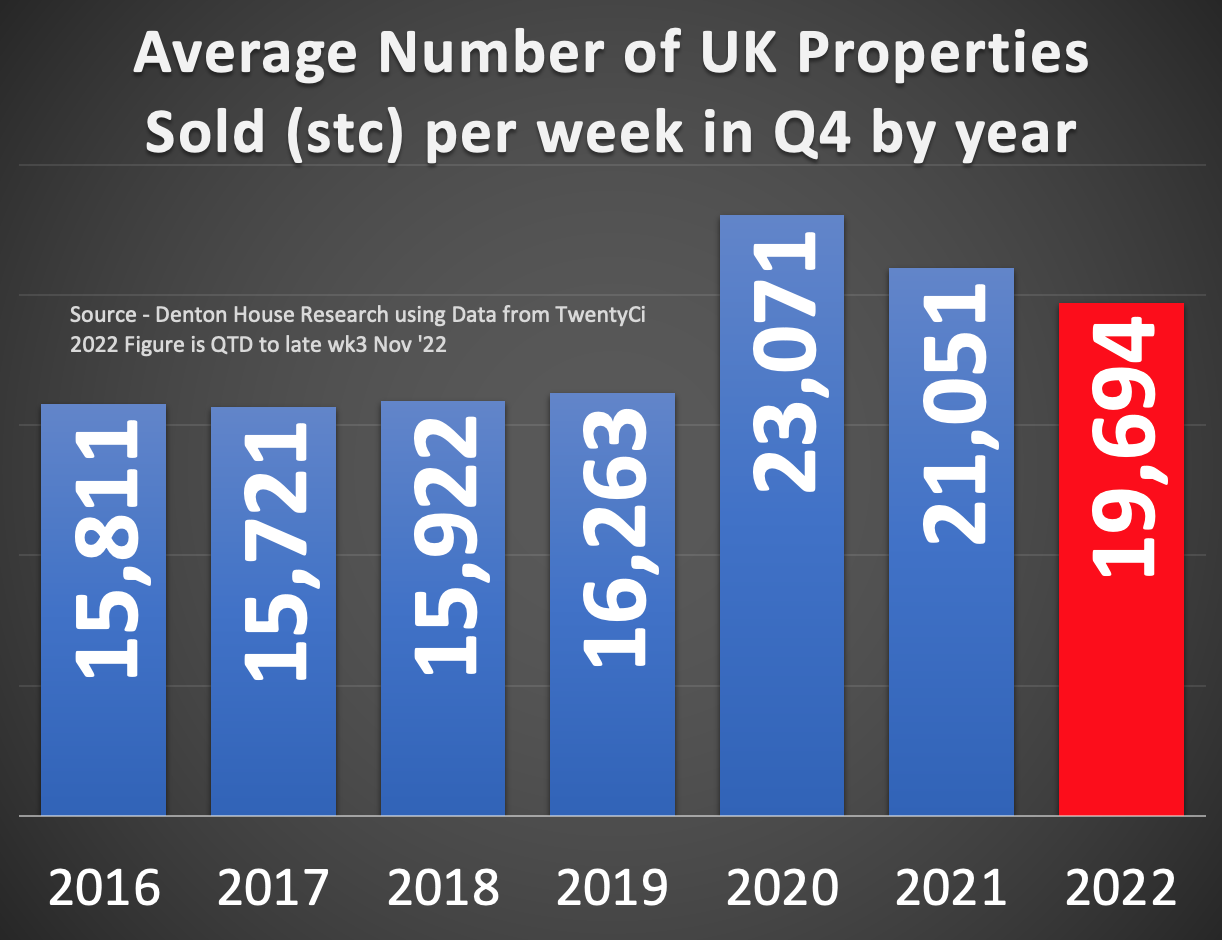

2020 and 2021 were exceptional years for the UK property market.

In Q4 2020 (Q4 being October, November, and December combined), an average of 23,071 properties were sold per week in the UK (sold – as in a sale was agreed and the property went from available to sold subject to contract (STC)).

In Q4 2021, an average of 21,051 properties were sold per week in the UK.

So, by the end of week 3 in November 2022, with an average of 19,694 properties per week becoming sold STC, quarter to date … the housing market doesn’t look good. Yet a different story emerges from the Q4 averages for 2016 to 2019.

- In Q4 2019, an average of 16,263 properties were sold per week

- In Q4 2018, an average of 15,922 properties were sold per week

- In Q4 2017, an average of 15,721 properties were sold per week

- In Q4 2016, an average of 15,811 properties were sold per week

“The British property market is only returning to how things were before the first lockdown.”

As I have discussed recently in several articles we have written and our market updates , the banks and economists predict when it comes to property prices achieved in the next 12-18 months, it expected to be between 6-10% less than was being paid for a property in the late spring (of 2022). Note I didn’t use the word ‘crash’.

Question – Why do the newspapers use the phrase “house price crash”?

Answer – To sell more newspapers!

Include the time, policy, and efforts that the political parties go to in order to keep British house prices on an upwards trajectory to gain votes and you might believe that a fall in house prices is a total catastrophe. Nothing could be further from the truth for most homeowners and landlords. Indeed, when you look at house prices without any emotion, when house prices fall — in isolation — more people win than lose.

Who wins when house prices drop?

Let’s say you own a two-bedroom Lancaster home worth £150,000. You have an expanding family, and you need a third bedroom.

The three-bedroom home in Lancaster you want is £230,000, meaning you need to find £80,000 to trade up.

If Lancaster house prices rose by 10%, get the Champagne on ice as your Lancaster two-bedroom home is now worth £165,000. Mind you before you open the fizzy stuff - remember the three-bed you want has also risen 10%, meaning it is now £253,000. If you want to trade up, you need to find £88,000.

Lancaster house prices rising has cost you an additional £8,000.

On the other side of the coin, what if Lancaster house prices fell 10%?

Your two-bedroom home is now only worth £135,000. Catastrophe! Yet wait — the three-bedroom Lancaster home you want to move up to is now worth £207,000, meaning you only need to find £72,000 to trade up.

Also, stamp duty, solicitor fees, and estate agent fees tend to be percentage based – thus saving you money.

As over 7 out of 10 home movers move up the property ladder, falling house prices are not necessarily a problem.

Falling Lancaster house prices are great for those who want to move up the property ladder and trade up.

Who loses when house prices drop?

The first set of people that lose out are homeowners moving down the market. The gap between selling a larger home and buying a smaller one narrows when one moves down market. Given the massive growth in house prices over many the decades those homeowners have been in the property market, it’s tough to see this as a calamity, yet it’s certainly a loss.

The second set of people that lose out are beneficiaries of the home being sold when a parent/grandparent passes away.

However, the most exposed (and many people will sympathise with these) are those first-time buyers who bought their first home with a small deposit. If you had just bought your first home for £200,000 with a 5% deposit (so you had a £190,000 mortgage) but Lancaster house prices dropped by 10%, you now own a home worth £180,000 (less than the mortgage). Now you are in ‘negative equity’ (as your mortgage is £10,000 more than what the house is worth, i.e., £190k less £180k), which causes you two main problems.

Firstly, when your fixed rate deal ends, most of the time, it is wise to re-mortgage to another rate. However, when you have negative equity, the range of mortgage deals open to you will be minimal, so you will probably have to pay your bank/building society’s quite pricey ‘standard variable rate’.

Secondly, suppose you want to sell your Lancaster home. In that case, the price you achieve will not pay off the mortgage, which means you will have to find the difference elsewhere (i.e. a gift/borrowing from your family or selling an asset like a car)—in a nutshell, making a move very difficult.

How many people will be drawn into negative equity if house prices drop 10%?

Just 2.9% of homeowners will be in negative equity, if house prices drop by 10%. Now of course, if you are one of that 2.9%, that will be challenging. Yet, the vast majority of those first-time buyers have been in their homes a year or less, and most first-time buyers only move to their second home after four to six years. Also, they will be fixed-rate mortgages (mostly five-year fixed-rate mortgages), so re-mortgaging won’t be an issue either.

But what would it mean to Lancaster house prices if they did drop by 10%?

If house prices drop by 10% in the next 12 months in Lancaster, that would only bring us back to the house prices being achieved in October 2021. If house prices dropped by the same percentage (19%) as they fell in the Credit Crunch in Lancaster, that would only bring us back to the house prices being achieved in August 2020. And nobody was complaining about those!

Let me get back to the real problem with falling house prices. When the country’s house prices fall, that tends to correspond with more challenging economic times. Now, because of rising interest rates and inflation, the price people are paying for a Lancaster property is lower than one would have paid in the spring (when you were bidding against multiple offers and had to pay a top price to secure the purchase).

However, when house prices dip , that can start to negatively affect the broader British economy. For some strange reason, homeowners tend to spend less because they ‘feel’ less well-off because the value of their home has dropped, and fewer people move home, meaning there is less choice for people to buy. Lenders start to be meaner about lending because they are nervous about arrears and bad debts building up.

2023 will be challenging for many Lancaster families, yet …

As we go into recession, the share of homeowners exposed to falling house prices is smaller than in the 2008 Credit Crunch.

- 92.48% of new mortgages taken out in the last four years have been fixed-rate mortgages, compared to 63.08% in the years before the Credit Crunch.

- In 2008, 45.4% of existing mortgages were 4% above the base rate, today, that is only 2.1%.

- Going into the Credit Crunch, the average mortgage rate homeowners were on was 5.88%, whilst the average rate existing mortgaged homeowners today are on is 2.17%.

Ultimately, unemployment is the main factor of whether this goes from being a possible 6- 10% decline to a full-scale crash.

If homeowners keep their jobs, they will keep paying their mortgages. However, (as in the 1988 and 2008 house price crash) if people lose their jobs, mortgages don’t tend to get paid, and that is when repossessions increase and forced selling starts to take effect.

However, looking back at the Autumn Statement, the Government has learned the lesson of previous generations and vastly improved the safety net of contributing to people’s mortgages. Should someone become unemployed, at the moment, homeowners must wait 39 weeks before the Government will help pay the mortgage (thus increasing their chances of repossession). This will be reduced to 12 weeks in the spring, reducing mortgage repossessions later in 2023/4.

So where does that leave us?

Personally I think we should be less keen to celebrate ‘house price booms’ throughout the ‘good times’ because the usual ‘house price crashes’ tend to worsen the ‘bad times’. In its place, we should concentrate on what British society can do to obtain a more stable property market over time.

Final thoughts: the house prices being achieved in late 2021/early 2022 in Lancaster will be a distant memory in a year’s time, yet for most people, that is not a bad thing. 2023 will be a challenging year, but don’t let the price paid for property by 3.54% of the UK population (the percentage of privately owned houses that will sell next year) affect your outlook and worth as a homeowner/landlord.

These are my thoughts – what are yours?

Thanks for reading this longer than normal article

Michelle x